Backtesting

Test any strategy configuration against historical data before risking real capital. The backtesting engine simulates order execution with realistic slippage, commission, and latency modeling across 180+ days of 1-minute candle data.

Setting Up a Backtest

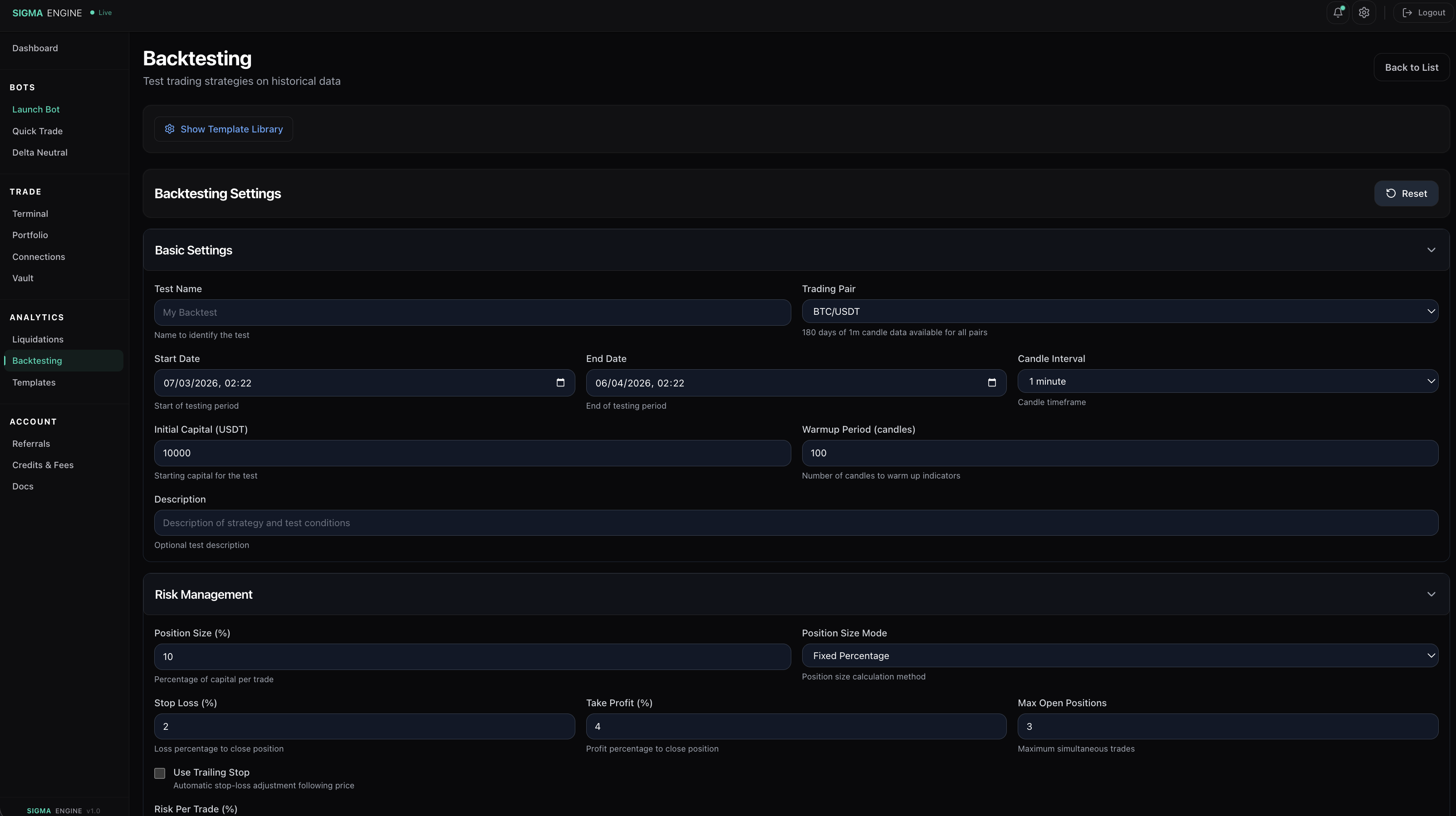

Basic Settings:

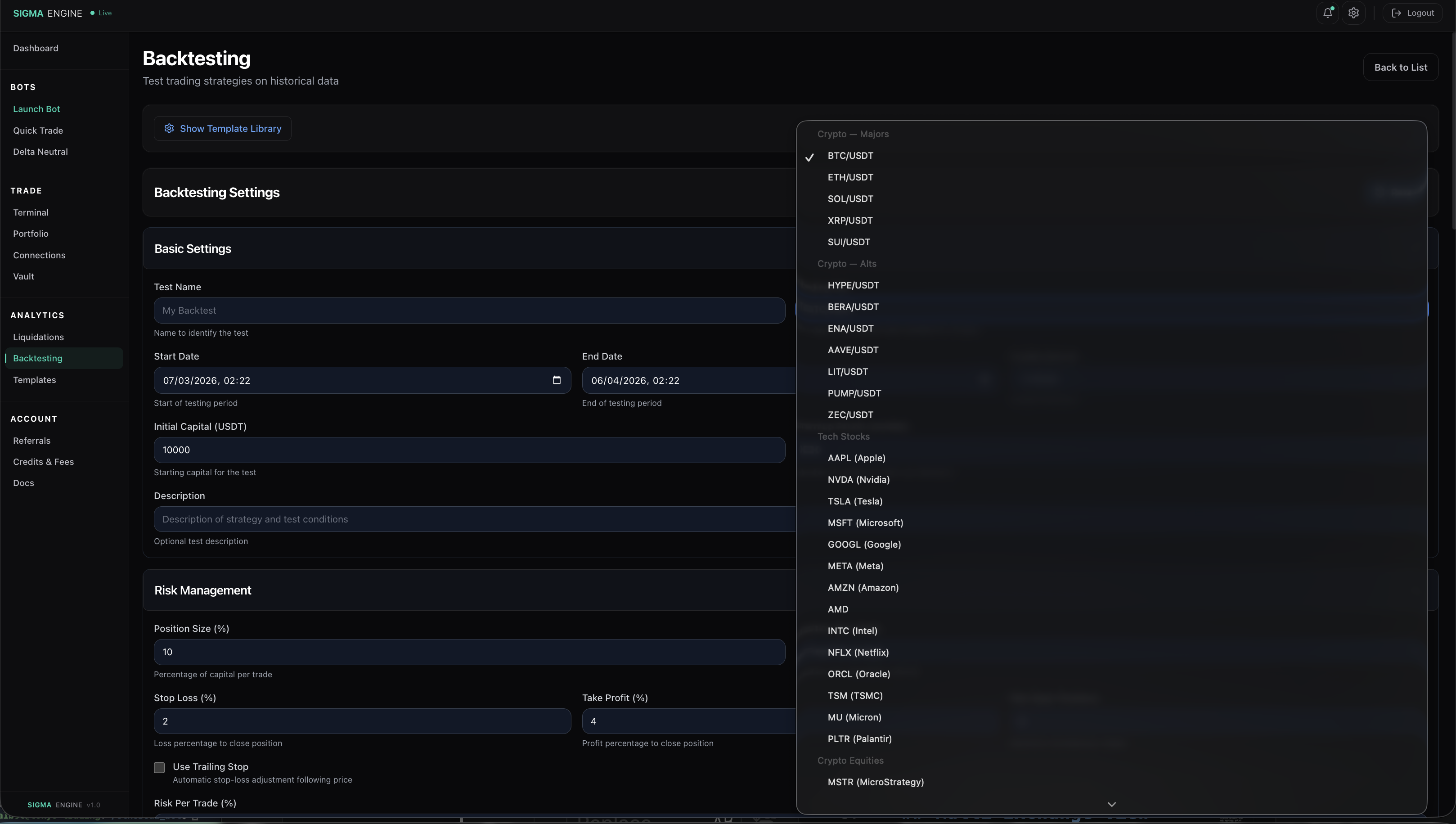

- Trading Pair - select from crypto majors, altcoins, tech stocks, commodities, and crypto-correlated equities

- Date Range - up to 180 days of 1-minute candle data available per pair

- Initial Capital - starting balance for the simulation

- Warmup Period - number of candles to feed indicators before the first signal fires (prevents cold-start trades on incomplete data)

Available Markets

Backtesting supports the same markets available for live trading:

- Crypto Majors - BTC, ETH, SOL, XRP, SUI

- Crypto Alts - HYPE, BERA, ENA, AAVE, LIT, PUMP, ZEC

- Tech Stocks - AAPL, NVDA, TSLA, MSFT, GOOGL, META, AMZN, AMD, INTC, NFLX, ORCL, TSM, MU, PLTR

- Crypto Equities - MSTR, COIN, HOOD, GME, RIVN

- Commodities - Gold, Silver, Brent Oil, Natural Gas, Copper, Platinum, Palladium, Uranium

All data is sourced from Binance Futures (crypto) and XYZ/Hyperliquid (stocks and commodities) at 1-minute resolution.

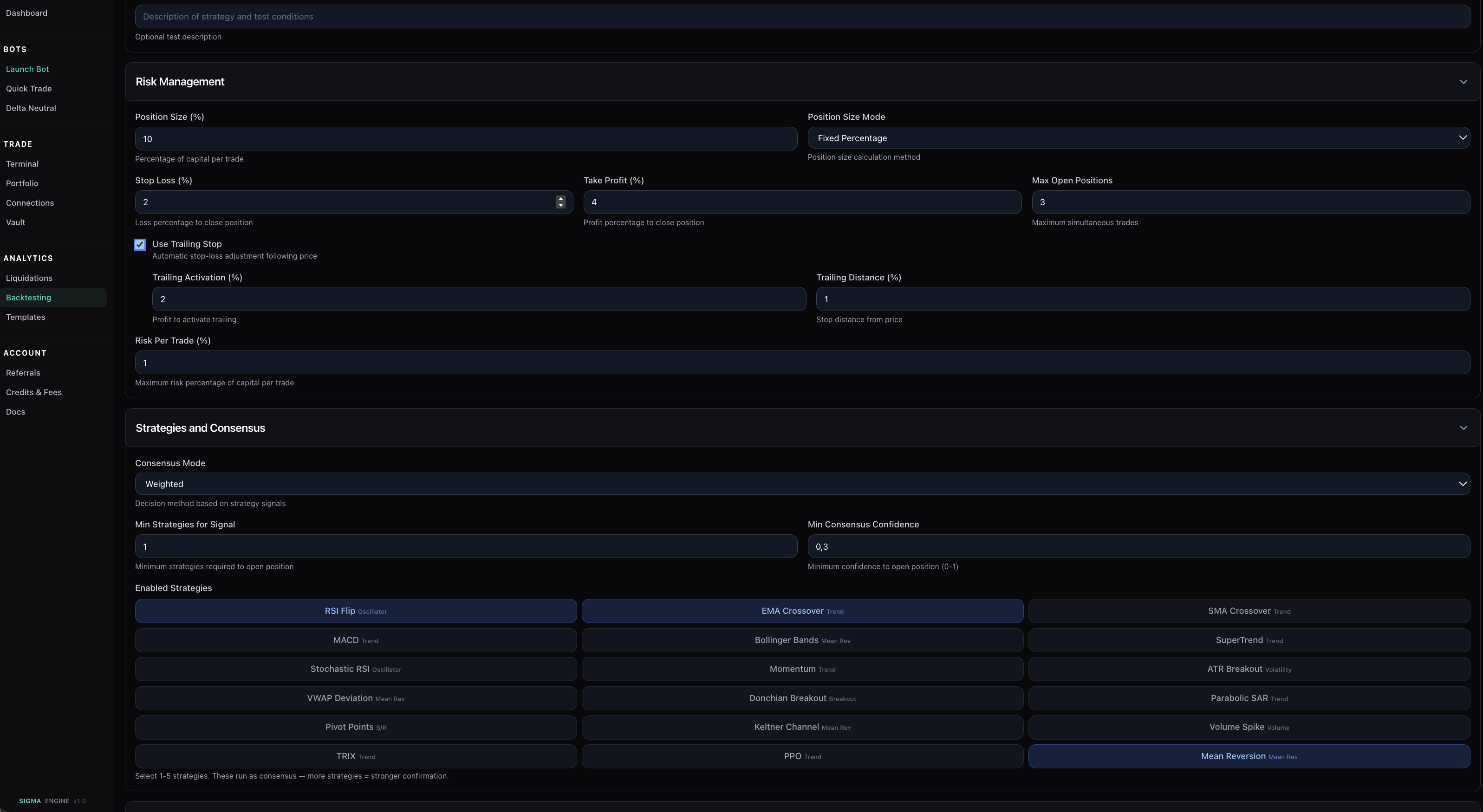

Risk Management

Configure position sizing, stop loss, take profit, trailing stops, and maximum concurrent positions. The risk management module runs identically in backtesting and live trading so results translate directly.

Strategies and Consensus - Select 1-5 technical analysis strategies that run as a consensus voting system. Each strategy produces an independent signal with a confidence score. The consensus engine aggregates these into a single direction and confidence level before any trade is taken.

Available strategies span oscillators (RSI Flip, Stochastic RSI), trend followers (EMA Crossover, MACD, SuperTrend, Parabolic SAR), mean reversion (Bollinger Bands, Keltner Channel, VWAP Deviation, Mean Reversion), breakout detectors (Donchian, ATR Breakout), and volume-based signals (Volume Spike, PPO, TRIX, Pivot Points).

More strategies selected means stronger confirmation requirements but fewer trades. Fewer strategies means more trades but weaker signal quality. The consensus mode (Weighted, Majority, Unanimous) controls how strict the agreement needs to be.

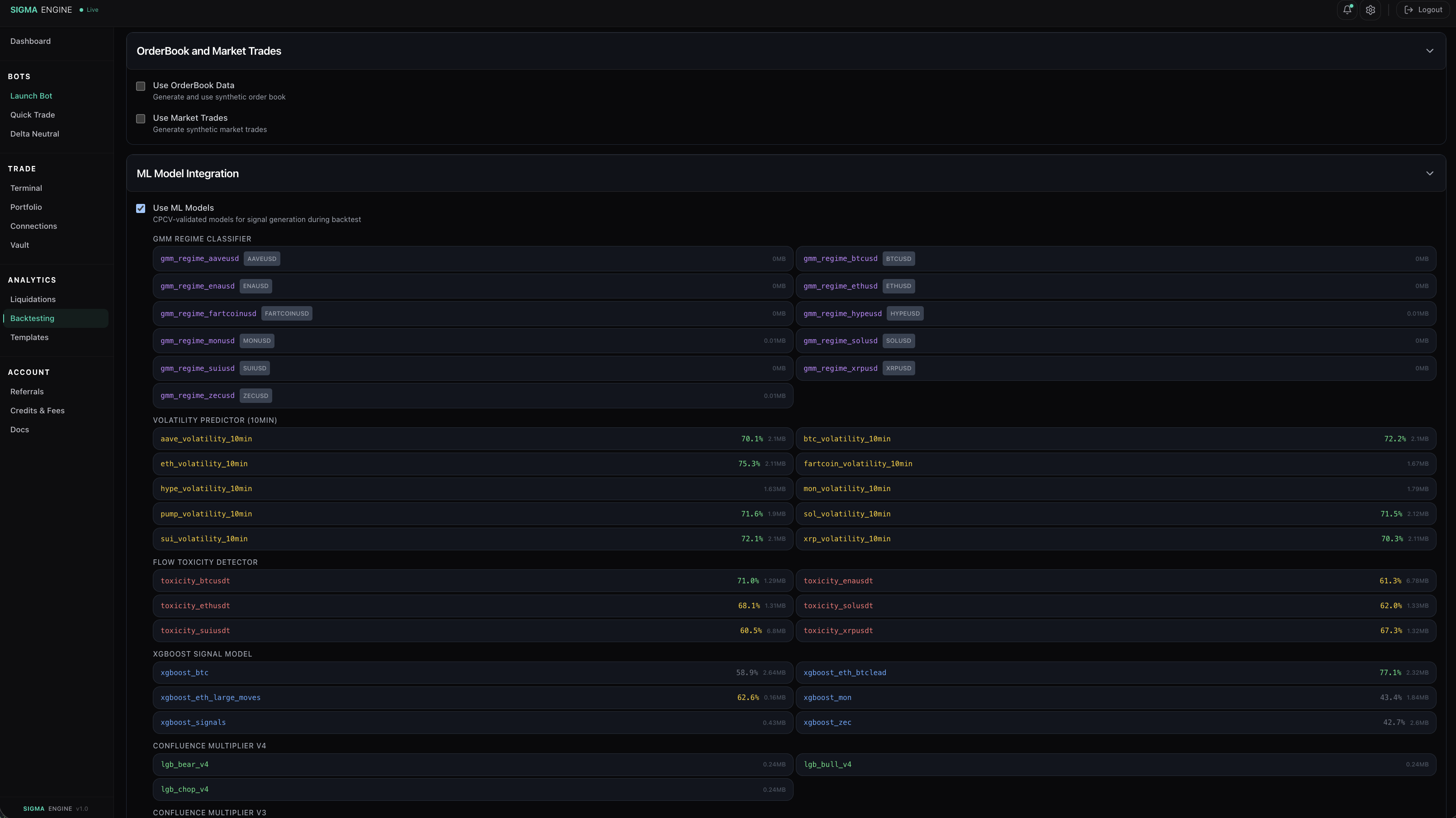

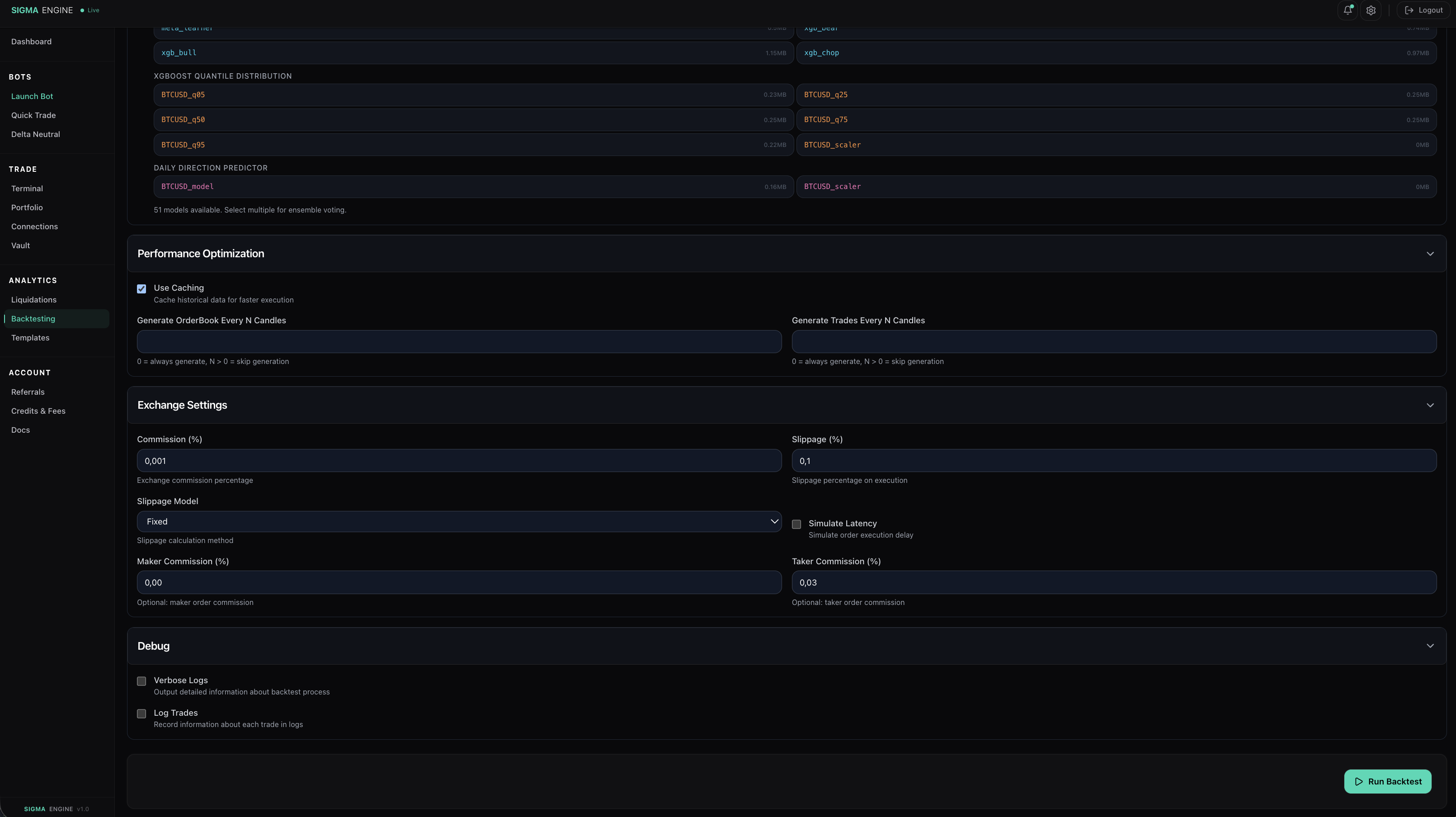

Machine Learning Models

The backtester integrates 51 pre-trained machine learning models organized into 8 categories. Each model was trained using Advances in Financial Machine Learning (AFML) methodology with Combinatorial Purged Cross-Validation (CPCV) to prevent overfitting.

Training methodology:

- All models trained on 365+ days of 1-minute candle data per asset

- CPCV with 6-10 purged folds ensures out-of-sample validation on every data point

- Walk-forward testing confirms performance degrades gracefully as market regimes shift

- Probability of Backtest Overfitting (PBO) computed per model to quantify look-ahead bias risk

- Models that failed PBO thresholds were discarded, not tuned

Model categories:

GMM Regime Classifier - Gaussian Mixture Models that identify the current market regime (trending, mean-reverting, or choppy) per coin. The backtester uses these to adapt strategy behavior based on detected conditions.

Volatility Predictor (10min) - Forecasts near-term realized volatility using a Corsi HAR-RV framework. Accuracy ranges from 70-75% across assets. Used by HAR-RV spread scaling in live bots.

Flow Toxicity Detector - Classifies order flow as informed (toxic) or uninformed using VPIN-derived features. Accuracy 61-71% per asset. When toxicity is elevated, the system widens spreads or pulls liquidity.

XGBoost Signal Models - Gradient-boosted trees trained on microstructure features (OBI, CVD, spread dynamics, funding rate). Per-coin models for BTC (58.9%), ETH-BTC lead (77.1%), and cross-asset signals.

Confluence Multiplier - LightGBM ensemble that combines multiple signal sources into a single confidence score. Separate bull/bear/chop classifiers weight each signal source by recent predictive accuracy.

XGBoost Ensemble - Meta-learner that aggregates outputs from individual models. Bull, bear, and chop sub-models vote, and the ensemble resolves conflicts.

Quantile Distribution - BTC-specific quantile regression models (Q05 through Q95) that estimate the probability distribution of returns over the next N candles. Used for dynamic take-profit and stop-loss placement.

Daily Direction Predictor - Longer-horizon model that predicts whether the next 24 hours will be net positive or negative. Used as a directional filter to suppress counter-trend entries.

Select multiple models for ensemble voting. The backtester applies them identically to how they run in live production, so backtest results reflect real model behavior.

Exchange Settings

Simulate realistic execution conditions:

- Commission - set maker and taker fees to match your target exchange (most DEXs: maker 0%, taker 0.02-0.05%)

- Slippage - fixed or variable slippage model to account for thin orderbooks

- Latency Simulation - optional delay between signal and execution to model real-world conditions

- Caching - historical data caching for faster re-runs when iterating on parameters

From Backtest to Template

When a backtest produces strong results, you can save the configuration as a template directly from the results page. Templates preserve every parameter: strategies, risk settings, ML model selection, and execution config.

Templates saved from backtesting start as private. You can deploy them to live trading via the Strategy Builder at any time. If you want to share a strategy that's proven profitable, you can publish it to the Template Marketplace.

How the marketplace works:

Publishing a template costs a one-time fee. In return, every time another user deploys your published template, you receive a payout. This creates a direct incentive to publish strategies that actually work in production. A template that backtests well and performs in live trading earns its creator ongoing revenue from each deployment.

The result is a flywheel: users who develop effective strategies are rewarded for sharing them. Users who want proven starting points can browse templates filtered by backtest metrics, community usage, and live performance data. Creators earn from real utility, not from subscriptions or paywalls. The better your template performs, the more it gets used, and the more you earn.

Templates that consistently underperform will naturally fall out of usage. Templates that consistently deliver will rise to the top and generate sustained income for their creators.

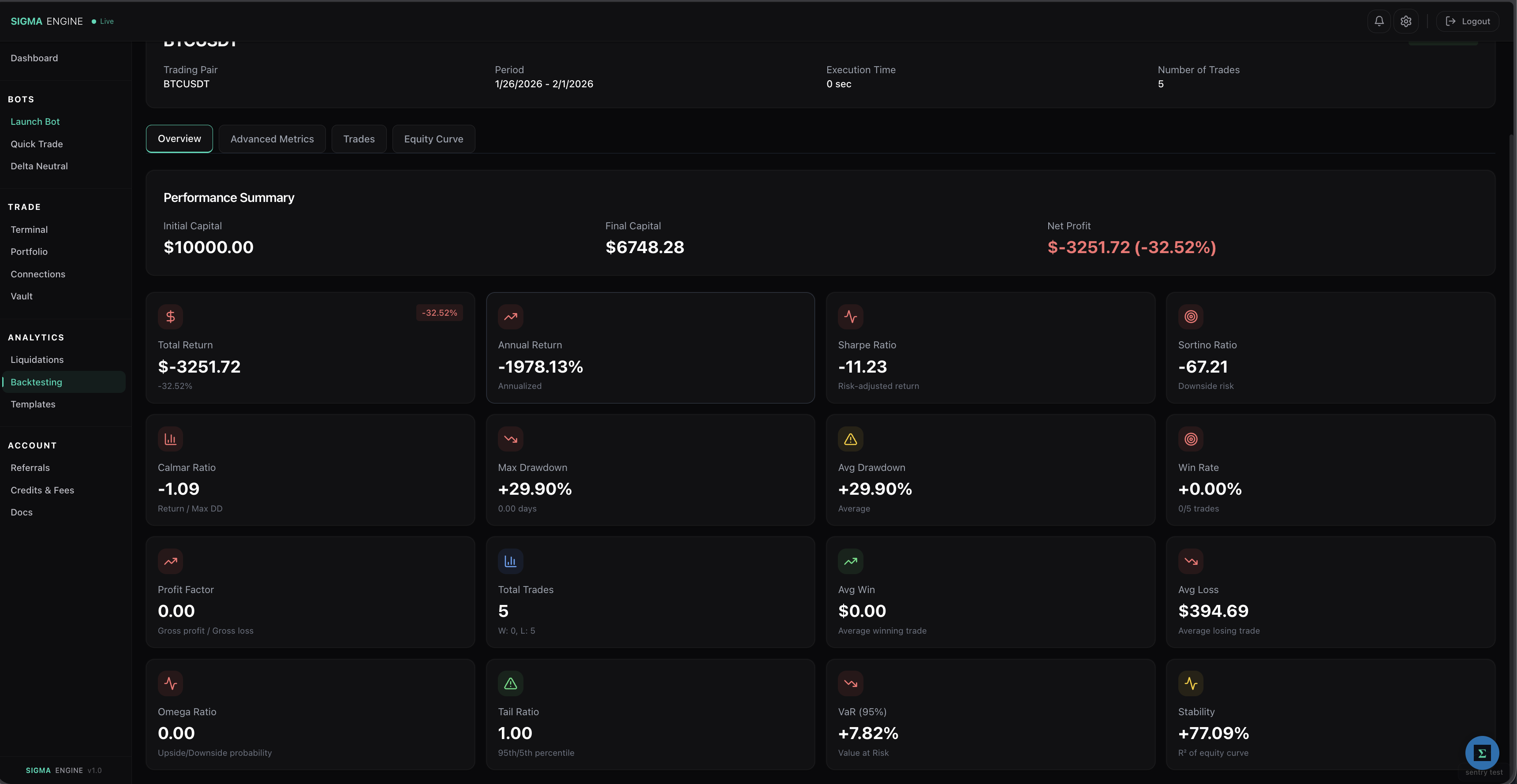

Backtest Results

After a backtest completes, results break down into four tabs:

- Overview — Total return, Sharpe ratio, Sortino ratio, max drawdown, win rate, profit factor, average win/loss

- Advanced Metrics — Risk-adjusted returns (Calmar, Omega), consistency (expectancy, Kelly criterion, win/loss streaks), drawdown analysis (duration, recovery factor), and market exposure

- Trades — Every entry and exit with direction, price, volume, PnL, duration, and exit reason (TP, SL, signal, end of backtest)

- Equity Curve — Portfolio value over time with peak, valley, and current markers

Use these to compare how different strategy combinations, ML models, position sizing modes, and risk parameters affect performance before going live.